Based on the factors that Benjamin Graham considered in analyzing potential stock picks, Kinder Morgan is not a quality investment. Only investors with a high risk tolerance and a solid investment thesis on the stock will be interested in this large-cap Oil & Gas Transportation and Processing company.

Kinder Morgan Trades at Fair Multiples

The “Graham number” is an equation that enables us to quickly determine how a stock is valued in terms of its earnings and assets:

√(22.5 * 6 year average earnings per share (0.6) * 6 year average book value per share (13.715) = $18.9

At today's price of $17.14 per share, Kinder Morgan is now trading -9.3% below price that Graham would recommend paying for the stock.

Some people use the Graham number alone, but it is best to consider it together with the other requirements for defensive stocks that Graham listed in Chapter 14 of The Intelligent Investor.

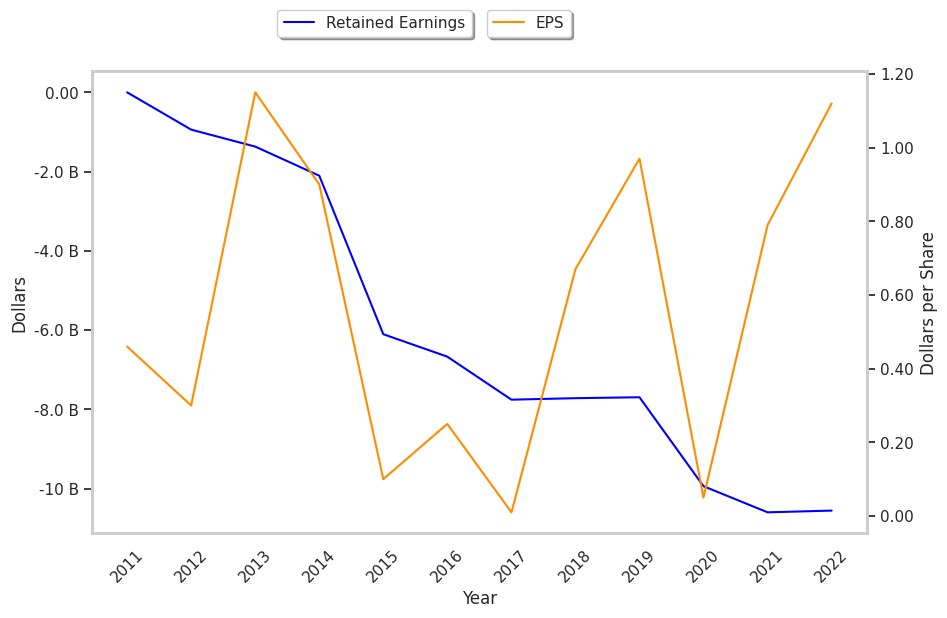

Negative Retained Earnings In 2019, 2020, And 2021, A Solid Record Of Dividends, and Decreasing Earnings Per Share

Ben Graham wrote that an investment in a company with a record of positive retained earnings could contribute significantly to the margin of safety. However, Kinder Morgan had negative retained earnings in 2019, 2020, and 2021 with an average of $-5495461538.461538 over this period.

Another one of Graham's requirements is for a 30% or more cumulative growth rate of the company's earnings per share over the last ten years.With only 9 years of available data, the Kinder Morgan cannot meet Graham's requirement of 30% growth over a 10 year period. Growth was disappointing during this period too. The average EPS during 2013 and 2014 was $1.02 based on the reported values of $1.15 and $0.89. Looking to the years 2021 and 2022, we see reported values of $0.78 and $1.12, which averages out to $0.95. This tells us that during this period Kinder Morgan's earnings per share shrank by -6.86%.

Shareholders of Kinder Morgan have received regular dividends since 2011. The company has returned an average dividend yield of 5.9% over the last five years.

Negative Current Asset to Liabilities Balance and Not Enough Current Assets to Cover Current Liabilities

Graham sought companies with extremely low debt levels compared to their assets. For one, he expected their current ratio to be over 2 and their long term debt to net current asset ratio to be near, or ideally under, under 1. Kinder Morgan fails on both counts with a current ratio of 0.6 and a debt to net current asset ratio of -0.8.

According to Graham's analysis, Kinder Morgan is likely a company of low quality, which is trading far above its fair price.

| 2018-02-09 | 2019-02-08 | 2020-02-12 | 2021-02-05 | 2022-02-07 | 2023-02-08 | |

|---|---|---|---|---|---|---|

| Revenue (MM) | $13,705 | $14,144 | $13,209 | $11,700 | $16,610 | $19,200 |

| Gross Margins | 68.0% | 69.0% | 75.0% | 78.0% | 61.0% | 52.0% |

| Operating Margins | 26% | 28% | 30% | 30% | 27% | 21% |

| Net Margins | 1.0% | 11.0% | 17.0% | 1.0% | 11.0% | 13.0% |

| Net Income (MM) | $183 | $1,609 | $2,190 | $119 | $1,784 | $2,548 |

| Net Interest Expense (MM) | -$1,832 | -$1,917 | -$1,801 | -$1,595 | -$1,492 | -$1,513 |

| Depreciation & Amort. (MM) | -$2,261 | -$2,297 | -$2,411 | -$2,164 | -$2,135 | -$2,186 |

| Earnings Per Share | $0.01 | $0.67 | $0.97 | $0.05 | $0.79 | $1.12 |

| EPS Growth | n/a | 6600.0% | 44.78% | -94.85% | 1480.0% | 41.77% |

| Diluted Shares (MM) | 2,230 | 2,216 | 2,264 | 2,263 | 2,267 | 2,265 |

| Free Cash Flow (MM) | $7,671 | $7,843 | $6,936 | $5,188 | $6,583 | $6,582 |

| Capital Expenditures (MM) | -$3,070 | -$2,800 | -$2,188 | -$638 | -$875 | -$1,615 |

| Net Current Assets (MM) | -$41,216 | -$37,947 | -$36,030 | -$36,204 | -$34,666 | -$34,161 |

| Long Term Debt (MM) | $33,988 | $33,105 | $30,883 | $30,838 | $29,772 | $28,288 |

| Net Debt / EBITDA | 6.3 | 5.31 | 5.09 | 5.7 | 4.69 | 4.97 |