Based on the factors that Benjamin Graham considered in analyzing potential stock picks, Tesla is not a quality investment. Only investors with a high risk tolerance and a solid investment thesis on the stock will be interested in this large-cap Auto Manufacturers company.

Tesla Is Probably Overvalued

Graham devised the below equation to give investors a quick way of determining whether a stock is trading at a fair multiple of its earnings and its assets:

√(22.5 * 6 year average earnings per share (0.68) * 6 year average book value per share (16.109) = $33.63

At today's price of $266.48 per share, Tesla is now trading 692.4% above the maximum price that Graham would have wanted to pay for the stock.

Even though the stock does not trade at an attractive multiple, it might still meet some of the other criteria for quality stocks that Graham listed in Chapter 14 of The Intelligent Investor.

Impressive Growth, but Inconsistent Profitability and no Dividend

Tesla’s average sales revenue over the last 6 years has been $40.15 Billion, so by Graham’s standards the company is large enough to warrant an investment. When published in 1972, Graham’s threshold was $100 million in average sales, which would be the equivalent of around a half million dollars today. Needless to say, this is the least important of Graham's requirements, and may be overlooked by all but the most conservative investors.

More importantly, Ben Graham believed that a margin of safety could be obtained by investing in companies with consistently positive retained earnings. Tesla had negative retained earnings in 2017, 2018, and 2019 with an average of $-1430842384.6153846 over this period. So the company is not accumulating enough cash over time by Graham's standards.

Graham also required a 30% or more cumulative growth rate of the company's earnings per share over the last ten years.There are only 8 years of EPS data available on Tesla, which is short of the required 10, but it's still worthwhile to consider its EPS trend over the available period. First, we will average out its EPS for 2015 and 2016 which were $-6.93 and $-4.68 respectively. This gives us an average of $-5.80 for the period of 2015 to 2016. Next, we compare this value with the average EPS reported in 2021 and 2022, which were $1.63 and $3.62, for an average of $2.62. Now we see that Tesla's EPS growth was 145.17% during this period, which satisfies Ben Graham's requirement for growth.

We have no record of Tesla offering a regular dividend.

Too Much Debt and an Average Current Ratio

Graham sought companies with extremely low debt levels compared to their assets. For one, he expected their current ratio to be over 2 and their long term debt to net current asset ratio to be near, or ideally under, under 1. Tesla fails on both counts with a current ratio of 1.5 and a debt to net current asset ratio of 0.4.

According to Graham's analysis, Tesla is likely a company of low quality, which is trading far above its fair price.

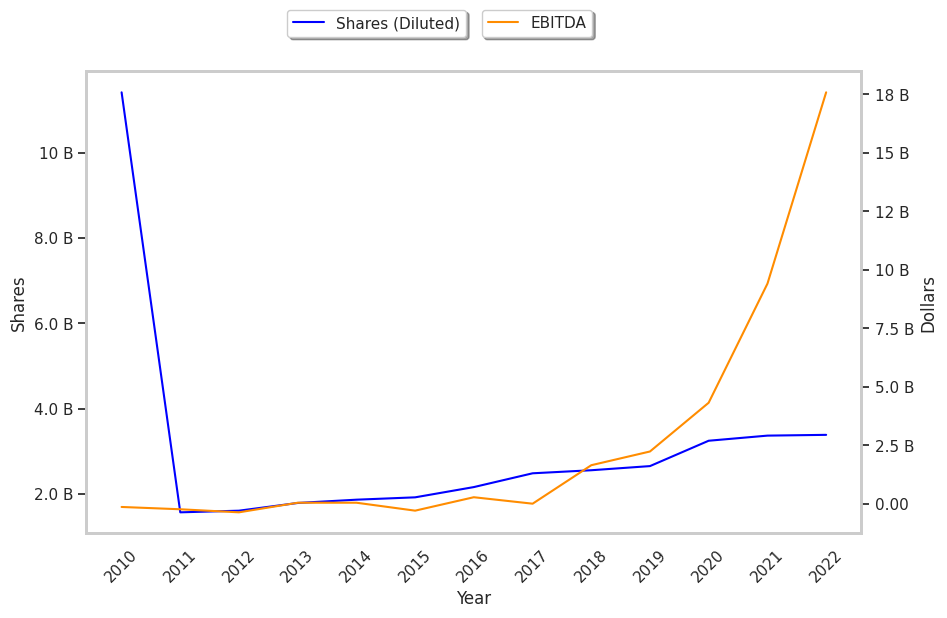

| 2018-02-23 | 2019-02-19 | 2020-04-28 | 2021-02-08 | 2022-02-07 | 2023-01-31 | |

|---|---|---|---|---|---|---|

| Revenue (MM) | $11,759 | $21,461 | $24,578 | $31,536 | $53,823 | $81,462 |

| Gross Margins | 19.0% | 19.0% | 17.0% | 21.0% | 25.0% | 26.0% |

| Operating Margins | -14% | -1% | 0% | 6% | 12% | 17% |

| Net Margins | -17.0% | -5.0% | -4.0% | 2.0% | 10.0% | 15.0% |

| Net Income (MM) | -$1,961 | -$976 | -$862 | $721 | $5,519 | $12,556 |

| Net Interest Expense (MM) | -$452 | -$639 | -$641 | -$718 | -$315 | $106 |

| Depreciation & Amort. (MM) | -$1,636 | -$1,901 | -$2,154 | -$2,322 | -$2,911 | -$3,747 |

| Earnings Per Share | -$0.79 | -$0.38 | -$0.32 | $0.22 | $1.64 | $3.71 |

| EPS Growth | n/a | 51.9% | 15.79% | 168.75% | 645.45% | 126.22% |

| Diluted Shares (MM) | 2,486 | 2,558 | 2,655 | 3,249 | 3,369 | 3,387 |

| Free Cash Flow (MM) | $4,021 | $4,417 | $3,842 | $9,185 | $18,011 | $21,896 |

| Capital Expenditures (MM) | -$4,081 | -$2,319 | -$1,437 | -$3,242 | -$6,514 | -$7,172 |

| Net Current Assets (MM) | -$16,452 | -$15,120 | -$14,096 | -$1,701 | -$3,448 | $4,477 |

| Long Term Debt (MM) | $9,418 | $9,404 | $11,634 | $9,556 | $5,245 | $1,597 |

| Net Debt / EBITDA | 1773.54 | 5.03 | 3.2 | -1.78 | -1.16 | -1.09 |