Standing out among the Street's worst performers today is TransUnion, a diversified financial company whose shares slumped -3.6% to a price of $47.94, 47.16% below its average analyst target price of $90.71.

The average analyst rating for the stock is buy. TRU lagged the S&P 500 index by -3.0% so far today and by -28.0% over the last year, returning -17.0%.

TransUnion operates as a global consumer credit reporting agency that provides risk and information solutions. The company is included in the financial services sector, which includes a wide variety of industries such as credit services, mortgage, banking, and insurance. Owing to this variety and the fast pace of innovation within these industries, investors may struggle to make sense of this sector.

As evidenced by the financial meltdown of 2008, seemingly healthy financial services companies — from insurers to investment banks — may see their market value plunge to zero in a matter of months. While the financial crash was likely a once-in-a-generation event, it highlights the volatility that is inherent to the sector. Financial innovation creates opportunities, but also new types of risk that investors and even the companies themselves may not fully understand.

TransUnion does not release its trailing 12 month P/E ratio since its earnings per share of $-1.35 are negative over the last year. But we can calculate it ourselves, which gives us a trailing P/E ratio for TRU of -35.5. Based on the company's positive earnings guidance of $4.23, the stock has a forward P/E ratio of 11.3. As of the first quarter of 2023, the average Price to Earnings (P/E) ratio for US finance companies is 14.34, and the S&P 500 has an average of 15.97. The P/E ratio consists in the stock's share price divided by its earnings per share (EPS), representing how much investors are willing to spend for each dollar of the company's earnings. Earnings are the company's revenues minus the cost of goods sold, overhead, and taxes.

It’s important to put the P/E ratio into context by dividing it by the company’s projected five-year growth rate. This results in the Price to Earnings Growth, or PEG ratio. Companies with comparatively high P/E ratios may still have a reasonable PEG ratio if their expected growth is strong. On the other hand, a company with low P/E ratios may not be of value to investors if it has low projected growth.

TransUnion's PEG ratio of 1.79 indicates that its P/E ratio is fair compared to its projected earnings growth. Insofar as its projected earnings growth rate turns out to be true, the company is probably fairly valued by this metric.

An analysis of the company's gross profit margins can help us understand its long term profitability and market position. Gross profits are the company's revenue minus the cost of goods only, and unlike earnings, don't take into account taxes and overhead. Here's an overview of TransUnion's gross profit margin trends:

| Date Reported | Revenue ($ k) | Cost of Revenue ($ k) | Gross Margins (%) | YoY Growth (%) |

|---|---|---|---|---|

| 2023 | 3,748,600 | 3,131,900 | 16 | -5.88 |

| 2022 | 3,709,900 | 3,079,300 | 17 | -22.73 |

| 2021 | 2,960,200 | 2,312,500 | 22 | 10.0 |

| 2020 | 2,530,600 | 2,030,400 | 20 | -9.09 |

| 2019 | 2,463,200 | 1,921,500 | 22 | 0.0 |

| 2018 | 2,317,200 | 1,804,700 | 22 |

- Average gross margin: 19.8 %

- Average gross margin growth rate: -4.7 %

- Coefficient of variability (lower numbers indicating more stability): 60.7 %

TransUnion's gross margins indicate that its underlying business is viable, and that the stock is potentially worthy for investment -- as opposed to speculative -- purposes.

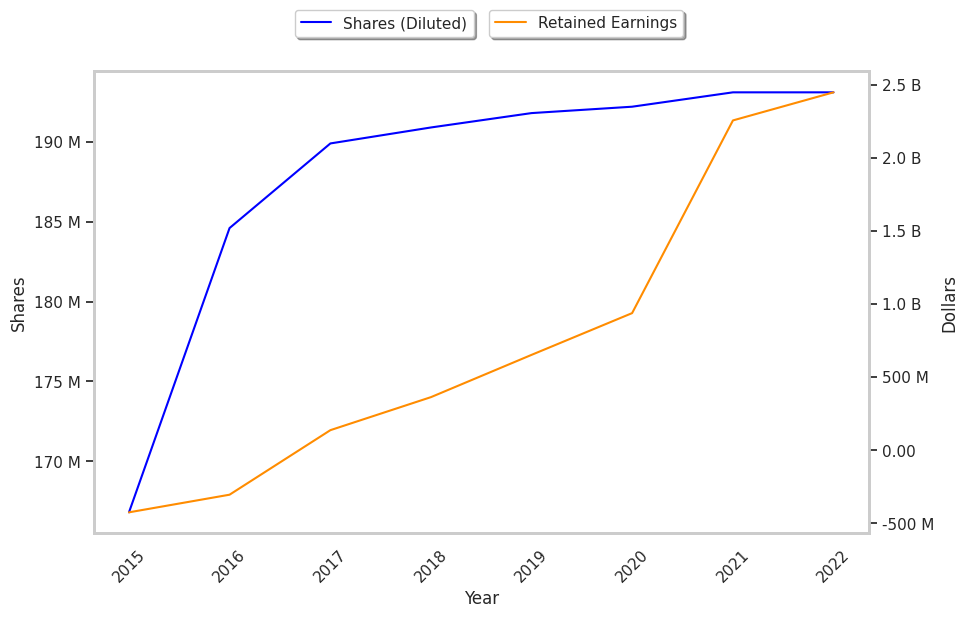

To deepen our understanding of the company's finances, we should study the effect of its depreciation and capital expenditures on the company's bottom line. We can see the effect of these additional factors in TransUnion's free cash flow, which was $388.8 Million as of its most recent annual report. The balance of cash flows represents the capital that is available for re-investment in the business, or for payouts to equity investors as dividends. The company's average cash flow over the last 4 years has been $420.92 Million and they've been growing at an average rate of 0.4%. TRU's weak free cash flow trend shows that it might not be able to sustain its dividend payments, which over the last 12 months has yielded 0.2% to investors. Cutting the dividend can compound a company's problems by causing investors to sell their shares, which further pushes down its stock price.

Another valuation metric for analyzing a stock is its Price to Book (P/B) Ratio, which consists in its share price divided by its book value per share. The book value refers to the present liquidation value of the company, as if it sold all of its assets and paid off all debts). Transunion's P/B ratio is 2.36 -- in other words, the market value of the company exceeds its book value by a factor of more than 2, so the company's assets may be overvalued compared to the average P/B ratio of the Finance sector, which stands at 1.57 as of the first quarter of 2023.

TransUnion is likely overvalued at today's prices because it has a negative P/E ratio, an average P/B ratio, and irregular cash flows with a flat trend. The stock has mixed growth prospects because of its decent operating margins with a stable trend, and a negative PEG ratio. We hope this preliminary analysis will encourage you to do your own research into TRU's fundamental values -- especially their trends over the last few years, which provide the clearest picture of the company's valuation.