Software company Zoom Video Communications stunned Wall Street today as it surged to $70.29, marking a 3.6% change compared to the S&P 500 and the Nasdaq indices, which logged 1.0% and 0.0% respectively. ZM is -8.26% below its average analyst target price of $76.62, which implies there is more upside for the stock. However, the average analayst rating for the stock is hold -- a more pessimistic outlook than you might expect. Over the last year, Zoom Video Communications has underperfomed the S&P 500 by 19.0%, moving -5.0%.

Zoom Video Communications, Inc. provides unified communications platform in the Americas, the Asia Pacific, Europe, the Middle East, and Africa. The companyis in the technology sector, which groups together a wide range of industries including consumer electronics, software, computer hardware, scientific instruments and IT services. Legendary investor Warren Buffet once stated that he would never invest in technology companies. Apple is now one of his largest holdings.

The risks inherent to the technology sector are clear, but investors simply cannot ignore the potential for strong returns. Even with the lessons learnt in the 2000 tech bubble, the market continues to highly value the promise of technological innovation and the ability for these companies to build and occupy new markets.

Zoom Video Communications's trailing 12 month P/E ratio is 92.5, based on its trailing EPS of $0.76. The company has a forward P/E ratio of 15.0 according to its forward EPS of $4.7 -- which is an estimate of what its earnings will look like in the next quarter. As of the first quarter of 2023, the average Price to Earnings (P/E) ratio of US technology companies is 27.16, and the S&P 500 average is 15.97. The P/E ratio consists in the stock's share price divided by its earnings per share (EPS), representing how much investors are willing to spend for each dollar of the company's earnings. Earnings are the company's revenues minus the cost of goods sold, overhead, and taxes.

Zoom Video Communications's P/E ratio tells us how much investors are willing to pay for each dollar of the company's earnings. The problem with this metric is that it doesn't take into account the expected growth in earnings of the stock. Sometimes elevated P/E ratios can be justified by equally elevated growth expectations.

We can solve this inconsistency by dividing the company's trailing P/E ratio by its five year earnings growth estimate, which in this case gives us a 9.15 Price to Earnings Growth (PEG) ratio. Since the PEG ratio is greater than 1, the company's lofty valuation is not completely justified by its growth levels.

To understand a company's long term business prospects, we must consider its gross profit margins, which is the ratio of its gross profits to its revenues. A wider gross profit margin indicates that a company may have a competitive advantage, as it is free to keep its product prices high relative to their cost. After looking at its annual reports, we obtained the following information on ZM's margins:

| Date Reported | Revenue ($ k) | Cost of Revenue ($ k) | Gross Margins (%) | YoY Growth (%) |

|---|---|---|---|---|

| 2023 | 4,392,960 | 3,047,080 | 31 | -40.38 |

| 2022 | 4,099,864 | 1,981,719 | 52 | -7.14 |

| 2021 | 2,651,368 | 1,169,531 | 56 | 166.67 |

| 2020 | 622,658 | 494,566 | 21 | 5.0 |

| 2019 | 330,517 | 263,349 | 20 |

- Average gross margin: 36.0 %

- Average gross margin growth rate: 8.9 %

- Coefficient of variability (higher numbers indicating more instability): 256.8 %

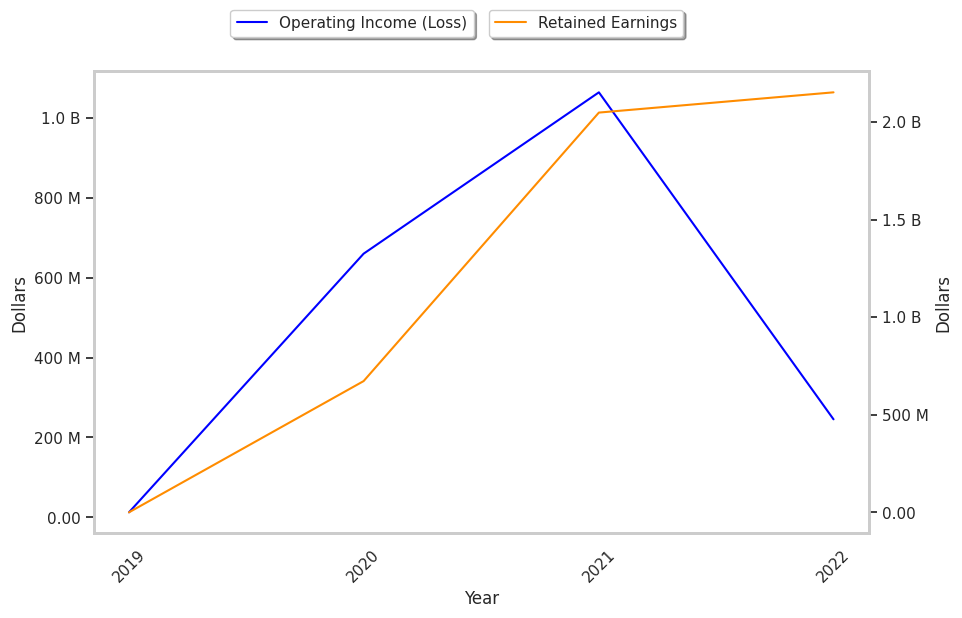

We can see from the above that Zoom Video Communications business is not strong and its stock is likely not suitable for conservative investors.

Another key to assessing a company's health is to look at its free cash flow, which is calculated on the basis of its total cash flow from operating activities minus its capital expenditures. Capital expenditures are the costs of maintaining fixed assets such as land, buildings, and equipment. From Zoom Video Communications's last four annual reports, we are able to obtain the following rundown of its free cash flow:

| Date Reported | Cash Flow from Operations ($ k) | Capital expenditures ($ k) | Free Cash Flow ($ k) | YoY Growth (%) |

|---|---|---|---|---|

| 2023 | 1,290,262 | 103,826 | 1,186,436 | -19.44 |

| 2022 | 1,605,266 | 132,590 | 1,472,676 | 5.86 |

| 2021 | 1,471,177 | 79,972 | 1,391,205 | 1122.41 |

| 2020 | 151,892 | 38,084 | 113,808 | 396.98 |

| 2019 | 51,332 | 28,432 | 22,900 |

- Average free cash flow: $837.4 Million

- Average free cash flow growth rate: 120.2 %

- Coefficient of variability (the lower the better): 176.8 %

Free cash flows represents the amount of money that is available for reinvesting in the business, or paying out to investors in the form of a dividend. With a positive cash flow as of the last fiscal year, ZM is in a position to do either -- which can encourage more investors to place their capital in the company.

Value investors often analyze stocks through the lens of its Price to Book (P/B) Ratio (its share price divided by its book value). As of the first quarter of 2023, the mean P/B ratio of the technology sector is 6.23, compared to the S&P 500 average of 2.95. The book value refers to the present value of the company if the company were to sell off all of its assets and pay all of its debts today - a number whose value may differ significantly depending on the accounting method. Zoom Video Communications's P/B ratio is 2.89, indicating that the market value of the company exceeds its book value by a factor of more than2, but is still below the average P/B ratio of the Technology sector.

Since it has an inflated P/E ratio, a lower P/B ratio than its sector average, generally positive cash flows on an upwards trend, Zoom Video Communications is likely fairly valued at today's prices. The company has poor growth indicators because of no PEG ratio and weak operating margins with a positive growth rate. We hope you enjoyed this basic overview of ZM's fundamentals. Make sure to check the numbers for yourself, especially focusing on their trends over the last few years.