Medical Specialities company Natera is taking Wall Street by surprise today, falling to $100.6 and marking a -8.9% change compared to the S&P 500, which moved -1.0%. NTRA is -19.59% below its average analyst target price of $125.11, which implies there is more upside for the stock.

As such, the average analyst rates it at buy. Over the last year, Natera shares have outstripped the S&P 500 by 109.4%, with a price change of 132.6%.

Natera, Inc., a diagnostics company, develops and commercializes molecular testing services worldwide. The company is categorized within the healthcare sector. The catalysts that drive valuations in this sector are complex. From demographics, regulations, scientific breakthroughs, to the emergence of new diseases, healthcare companies see their prices swing on the basis of a variety of factors.

Natera does not publish either its forward or trailing P/E ratios because their values are negative -- meaning that each share of stock represents a net earnings loss. But we can calculate these P/E ratios anyways using the stocks forward and trailing (EPS) values of $-1.19 and $-3.11. We can see that NTRA has a forward P/E ratio of -84.5 and a trailing P/E ratio of -32.3. As of the second quarter of 2024, the average Price to Earnings (P/E) ratio for US health care companies is 27.61, and the S&P 500 has an average of 28.21. The P/E ratio consists in the stock's share price divided by its earnings per share (EPS), representing how much investors are willing to spend for each dollar of the company's earnings. Earnings are the company's revenues minus the cost of goods sold, overhead, and taxes.

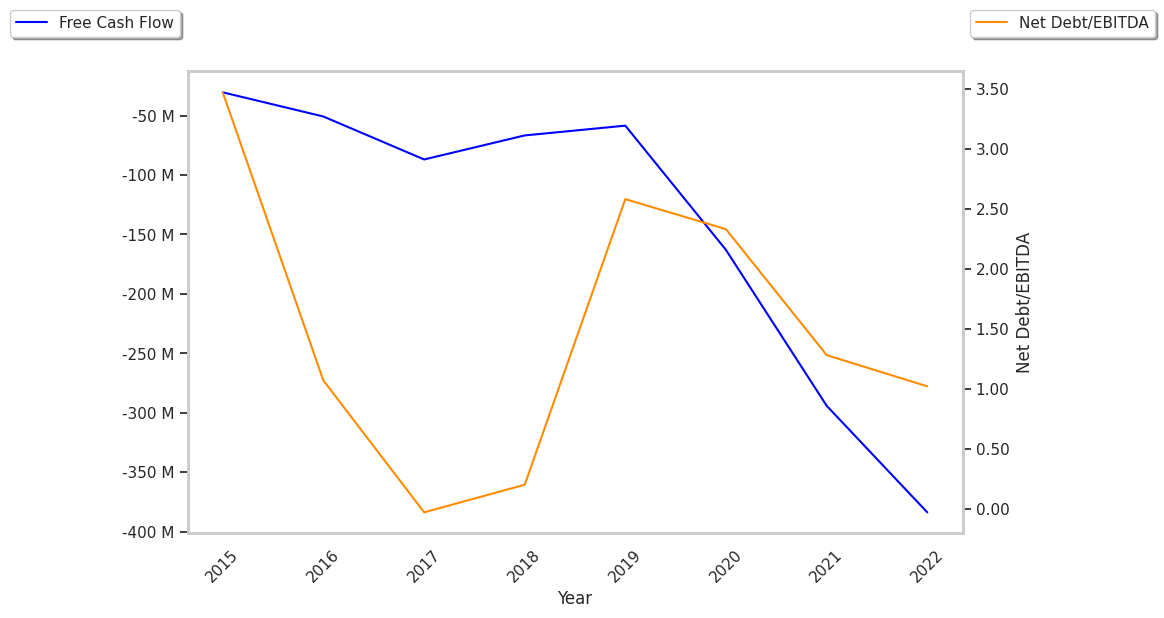

When we subtract capital expenditures from operating cash flows, we are left with the company's free cash flow, which for Natera was $-286154000 as of its last annual report. Free cash flow represents the amount of money available for reinvestment in the business or for payments to equity investors in the form of a dividend. In NTRA's case the cash flow outlook is weak. It's average cash flow over the last 4 years has been $-247767833.3 and they've been growing at an average rate of -32.0%.

Value investors often analyze stocks through the lens of its Price to Book (P/B) Ratio (its share price divided by its book value). The book value refers to the present value of the company if the company were to sell off all of its assets and pay all of its debts today - a number whose value may differ significantly depending on the accounting method. Natera's P/B ratio is 15.48 -- in other words, the market value of the company exceeds its book value by a factor of more than 15, so the company's assets may be overvalued compared to the average P/B ratio of the Health Care sector, which stands at 3.69 as of the second quarter of 2024.

Natera is likely fairly valued at today's prices because it has a negative P/E ratio., a higher than Average P/B Ratio, and negative cash flows with a downwards trend. The stock has poor growth indicators because of its weak operating margins with a stable trend, and no PEG ratio. We hope this preliminary analysis will encourage you to do your own research into NTRA's fundamental values -- especially their trends over the last few years, which provide the clearest picture of the company's valuation.