Oil & Gas Integrated company Marathon Petroleum is standing out today, surging to $156.41 and marking a 6.4% change. In comparison the S&P 500 moved only 1.0%. MPC is -6.16% below its average analyst target price of $166.68, which implies there is more upside for the stock.

As such, the average analyst rates it at buy. Over the last year, Marathon Petroleum has underperfomed the S&P 500 by 32.8%, moving -11.8%.

Marathon Petroleum Corporation, together with its subsidiaries, operates as an integrated downstream energy company primarily in the United States. The company is classified within the energy sector. The stock prices of energy companies are highly correlated with geopolitics: economic crisis, war, commodity prices, and politics all have an effect on the industry. For this reason, energy companies tend to have high volatility --- meaning large and frequent price swings. As global energy supplies shift towards renewables, we may see a reduced correlation between energy prices and geopolitical events.

Marathon Petroleum's trailing 12 month P/E ratio is 12.1, based on its trailing EPS of $12.89. The company has a forward P/E ratio of 12.6 according to its forward EPS of $10.2 -- which is an estimate of what its earnings will look like in the next quarter.

As of the third quarter of 2024, the average Price to Earnings (P/E) ratio for US energy companies is 13.62, and the S&P 500 has an average of 29.3. The P/E ratio consists in the stock's share price divided by its earnings per share (EPS), representing how much investors are willing to spend for each dollar of the company's earnings. Earnings are the company's revenues minus the cost of goods sold, overhead, and taxes.

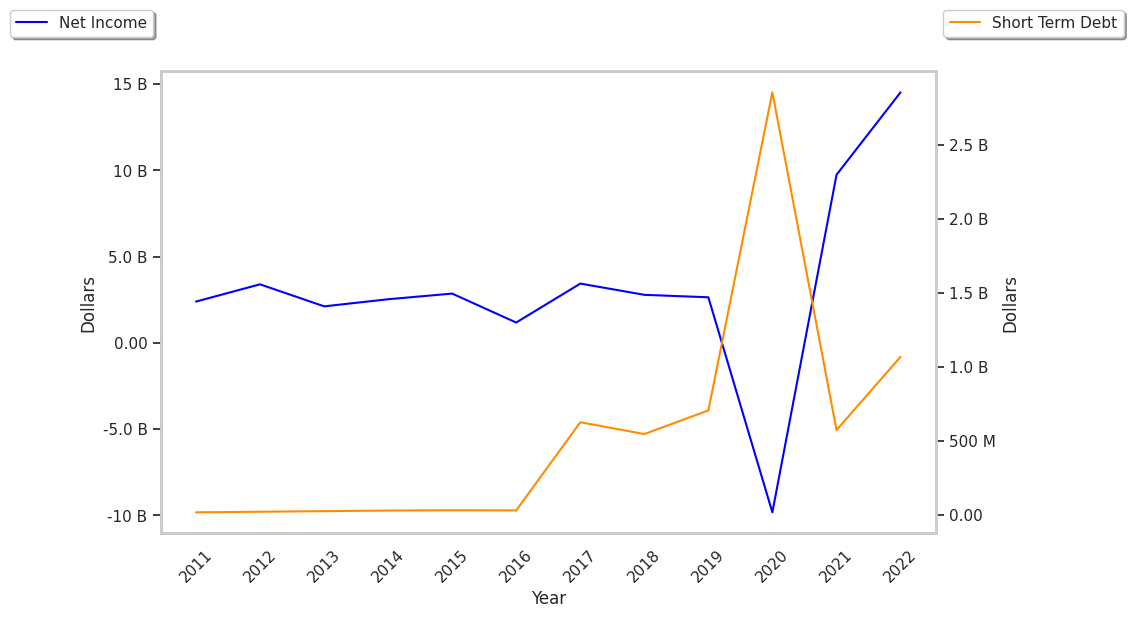

Marathon Petroleum's financial viability can also be assessed through a review of its free cash flow trends. Free cash flow refers to the company's operating cash flows minus its capital expenditures, which are expenses related to the maintenance of fixed assets such as land, infrastructure, and equipment. Over the last four years, the trends have been as follows:

| Date Reported | Cash Flow from Operations ($ k) | Capital expenditures ($ k) | Free Cash Flow ($ k) | YoY Growth (%) |

|---|---|---|---|---|

| 2023 | 14,117,000 | 1,890,000 | 12,227,000 | -12.29 |

| 2022 | 16,361,000 | 2,420,000 | 13,941,000 | 381.39 |

| 2021 | 4,360,000 | 1,464,000 | 2,896,000 | 886.96 |

| 2020 | 2,419,000 | 2,787,000 | -368,000 | -107.95 |

| 2019 | 9,441,000 | 4,810,000 | 4,631,000 | 55.45 |

| 2018 | 6,158,000 | 3,179,000 | 2,979,000 |

- Average free cash flow: $6.05 Billion

- Average free cash flown growth rate: 26.3 %

- Coefficient of variability (lower numbers indicating more stability): 0.0 %

With its positive cash flow, the company can not only re-invest in its business, it can offer regular returns to its equity investors in the form of dividends. Over the last 12 months, investors in MPC have received an annualized dividend yield of 2.3% on their capital.

Another valuation metric for analyzing a stock is its Price to Book (P/B) Ratio, which consists in its share price divided by its book value per share. The book value refers to the present liquidation value of the company, as if it sold all of its assets and paid off all debts.

Marathon Petroleum's P/B ratio indicates that the market value of the company exceeds its book value by a factor of 2, so the company's assets may be overvalued compared to the average P/B ratio of the Energy sector, which stands at 1.86 as of the third quarter of 2024.

Marathon Petroleum is by most measures undervalued because it has a Very low P/E ratio, an average P/B ratio, and generally positive cash flows with an upwards trend. The stock has mixed growth prospects because it has a an average PEG ratio and weak operating margins with a positive growth rate. We hope you enjoyed this overview of MPC's fundamentals.