Specialty Retail company Bath & Body Works is standing out today, surging to $36.99 and marking a 4.9% change. In comparison the S&P 500 moved only -0.0%. BBWI is -7.27% below its average analyst target price of $39.89, which implies there is more upside for the stock.

As such, the average analyst rates it at buy. Over the last year, Bath & Body Works has underperfomed the S&P 500 by 31.0%, moving -14.0%.

Bath & Body Works, Inc. operates a specialty retailer of home fragrance, body care, and soaps and sanitizer products. The company None

Bath & Body Works's trailing 12 month P/E ratio is 11.7, based on its trailing EPS of $3.15. The company has a forward P/E ratio of 11.2 according to its forward EPS of $3.29 -- which is an estimate of what its earnings will look like in the next quarter.

The P/E ratio is the company's share price divided by its earnings per share. In other words, it represents how much investors are willing to spend for each dollar of the company's earnings (revenues minus the cost of goods sold, taxes, and overhead). As of the first quarter of 2023, the consumer cyclical sector has an average P/E ratio of 22.96, and the average for the S&P 500 is 15.97.

BBWI’s price to earnings ratio can be divided by its projected five-year growth rate, to give us the price to earnings, or PEG ratio. This allows us to put its earnings valuation in the context of its growth expectations which is useful because companies with low P/E ratios often have low growth, which means they actually do not present an attractive value.

When we perform the calculation for Bath & Body Works, we obtain a PEG ratio of 2.87, which indicates that the company is overvalued compared to its growth prospects. The weakness with PEG ratios is that they rely on expected growth estimates, which of course may not turn out as expected.

To gauge the health of Bath & Body Works's underlying business, let's look at gross profit margins, which are the company's revenue minus the cost of goods only. Analyzing gross profit margins gives us a good picture of the company's pure profit potential and pricing power in its market, unclouded by other factors. As such, it can provide insights into the company's competitive advantages -- or lack thereof.

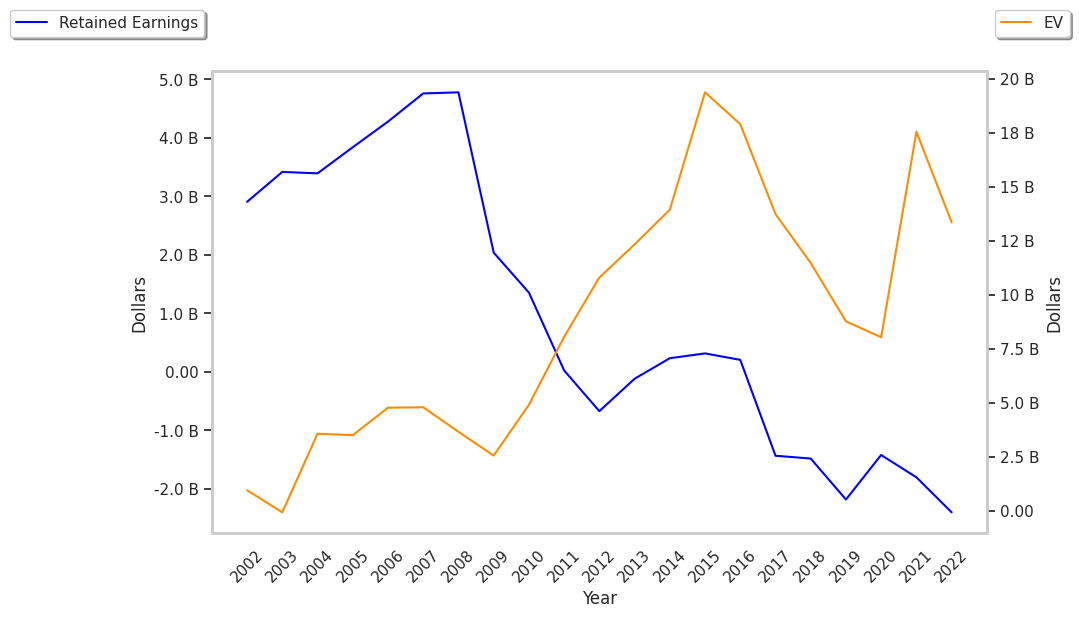

BBWI's average gross profit margins over the last four years are 43.3%, which indicate it has a potential competitive advantage in its market. These margins have slightly increased over the last four years, with an average growth rate of 1.7%. Another key to assessing a company's health is to look at its free cash flow, which is calculated on the basis of its total cash flow from operating activities minus its capital expenditures. Capital expenditures are the costs of maintaining fixed assets such as land, buildings, and equipment. From Bath & Body Works's last four annual reports, we are able to obtain the following rundown of its free cash flow:

| Date Reported | Cash Flow from Operations ($ k) | Capital expenditures ($ k) | Free Cash Flow ($ k) | YoY Growth (%) |

|---|---|---|---|---|

| 2023 | 1,144,000 | 328,000 | 816,000 | -33.22 |

| 2022 | 1,492,000 | 270,000 | 1,222,000 | -32.52 |

| 2021 | 2,039,000 | 228,000 | 1,811,000 | 132.78 |

| 2020 | 1,236,000 | 458,000 | 778,000 | 4.01 |

| 2019 | 1,377,000 | 629,000 | 748,000 | 7.01 |

| 2018 | 1,406,000 | 707,000 | 699,000 |

- Average free cash flow: $1.01 Billion

- Average free cash flown growth rate: 2.6 %

- Coefficient of variability (the lower the better): 524.7 %

With its positive cash flow, the company can not only re-invest in its business, it can offer regular returns to its equity investors in the form of dividends. Over the last 12 months, investors in BBWI have received an annualized dividend yield of 2.3% on their capital.

Bath & Body Works is by most measures overvalued because it has a very low P/E ratio, no published P/B ratio, and irregular cash flows with a flat trend. The stock has poor growth indicators because it has a an inflated PEG ratio and decent operating margins with a stable trend. We hope you enjoyed this overview of BBWI's fundamentals.