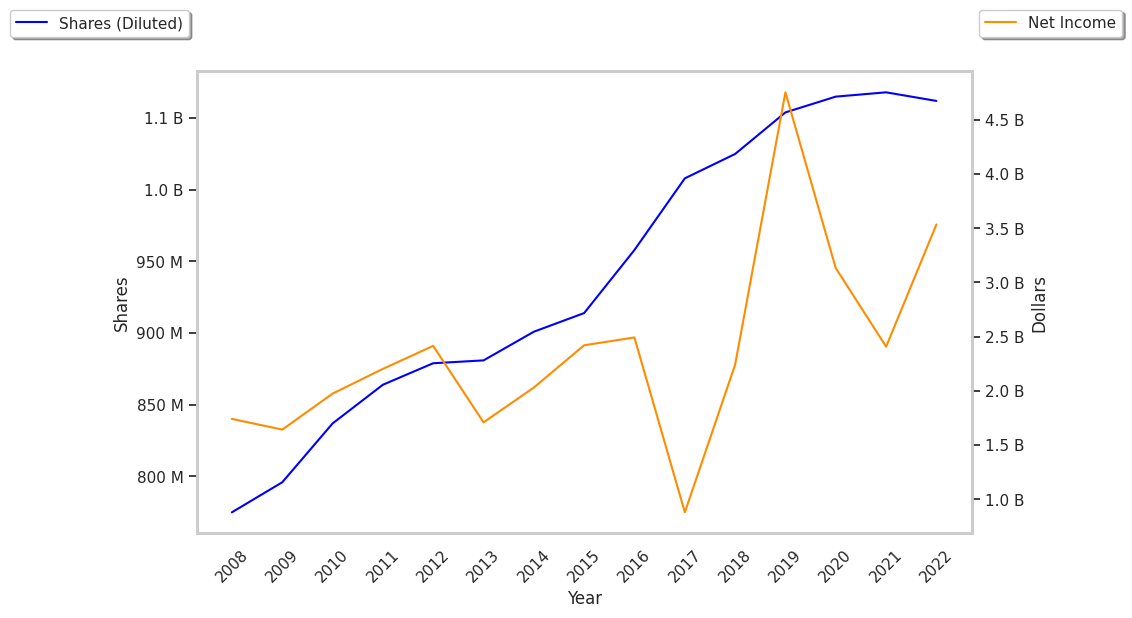

With an average analyst rating of buy, Southern is clearly an analyst favorite. But the analysts could be wrong. Is SO overvalued at today's price of $79.55? Let's take a closer look at the fundamentals to find out.

The first step in determining whether a stock is overvalued is to check its price to book (P/B) ratio. This is perhaps the most basic measure of a company's valuation, which is its market value divided by its book value. Book value refers to the sum of all of the company's assets minus its liabilities -- you can also think of it as the company's equity value.

Traditionally, value investors would look for companies with a ratio of less than 1 (meaning that the market value was smaller than the company's book value), but such opportunities are very rare these days. So we tend to look for company's whose valuations are less than their sector and market average. The P/B ratio for Southern is 2.72, compared to its sector average of 2.27 and the S&P 500's average P/B of 4.59.

Modernly, the most common metric for valuing a company is its Price to Earnings (P/E) ratio. It's simply today's stock price of 79.55 divided by either its trailing or forward earnings, which for Southern are $3.86 and $4.32 respectively. Based on these values, the company's trailing P/E ratio is 20.6 and its forward P/E ratio is 18.4. By way of comparison, the average P/E ratio of the Utilities sector is 20.35 and the average P/E ratio of the S&P 500 is 27.65.

The problem with P/E ratios is that they don't take into account the growth of earnings. This means that a company with a higher than average P/E ratio may still be undervalued if it has extremely high projected earnings growth. Conversely, a company with a low P/E ratio may not present a good value proposition if its projected earnings are stagnant.

When we divide Southern's P/E ratio by its projected 5 year earnings growth rate, we obtain its Price to Earnings Growth (PEG) ratio of 2.75. Since a PEG ratio between 0 and 1 may indicate that the company's valuation is proportionate to its growth potential, we see here that SO is overvalued when we factor growth into the price to earnings calculus. One important caveat here is that PEG ratios are calculated on the basis of future earnings growth estimates, which may turn out to be wrong.

If a company is overvalued in terms of its earnings, we also need to check if it has the ability to meet its financial obligations. One way to check this is via the so called Quick Ratio or Acid Test, which is the sum of its current assets, inventory, and prepaid expenses divided by its current liabilities. Southern's Quick ratio is 0.407, which indicates that that it does not have the liquidity necessary to meet its current liabilities.

Investors are undoubtedly attracted by Southern's dividend of $3.5%. But can the company keep up these payments? Dividends are paid out from levered free cash flow, which is the money left over after the company has accounted for all expenses and income -- including those unrelated to its core business. In Southern's case, the cash flows are negative which calls into question the firm's ability to sustain its dividends.

Analysts are bullish on Southern, but we are concerned they may be missing the clouded growth picture, as expressed by the stock's elevated PEG ratio. In addition, many of its valuation metrics point to a stock with an inflated value. We will keep following SO to see whether the analyst community was right.