Standing out among the Street's worst performers today is Freeport-McMoRan, a industrial metals & mining company whose shares slumped -3.9% to a price of $49.27, 9.61% below its average analyst target price of $54.51.

The average analyst rating for the stock is buy. FCX underperformed the S&P 500 index by -4.0% during today's afternoon session, but outpaced it by 7.0% over the last year with a return of 30.3%.

Freeport-McMoRan Inc. engages in the mining of mineral properties in North America, South America, and Indonesia. The company belongs to the basic materials sector, which includes the chemical, coal, mining, aluminum, and steel industries. The demand for these materials is dependent on economic cycles: when the economy is growing, companies across all sectors ramp up production, which increases demand from basic materials companies.

Conversely, when the economy slows down, demand for these materials decreases. The stock prices of this sector tend to follow the ebbs and flows of these demand cycles — but accurately predicting where we are presently in the economic cycle is a matter of intense debate.

Freeport-McMoRan's trailing 12 month P/E ratio is 43.2, based on its trailing EPS of $1.14. The company has a forward P/E ratio of 21.8 according to its forward EPS of $2.26 -- which is an estimate of what its earnings will look like in the next quarter. As of the second quarter of 2024, the average Price to Earnings (P/E) ratio for US basic materials companies is 22.71, and the S&P 500 has an average of 27.65. The P/E ratio consists in the stock's share price divided by its earnings per share (EPS), representing how much investors are willing to spend for each dollar of the company's earnings. Earnings are the company's revenues minus the cost of goods sold, overhead, and taxes.

To better understand FCX’s valuation, we can divide its price to earnings ratio by its projected five-year growth rate, which gives us its price to earnings, or PEG ratio. Considering the P/E ratio in the context of growth is important, because many companies that are undervalued in terms of earnings are actually overvalued in terms of growth.

Freeport-McMoRan’s PEG is 3.0, which indicates that the company is overvalued compared to its growth prospects. Bear in mind that PEG ratios have limits to their relevance, since they are based on future growth estimates that may not turn out as expected.

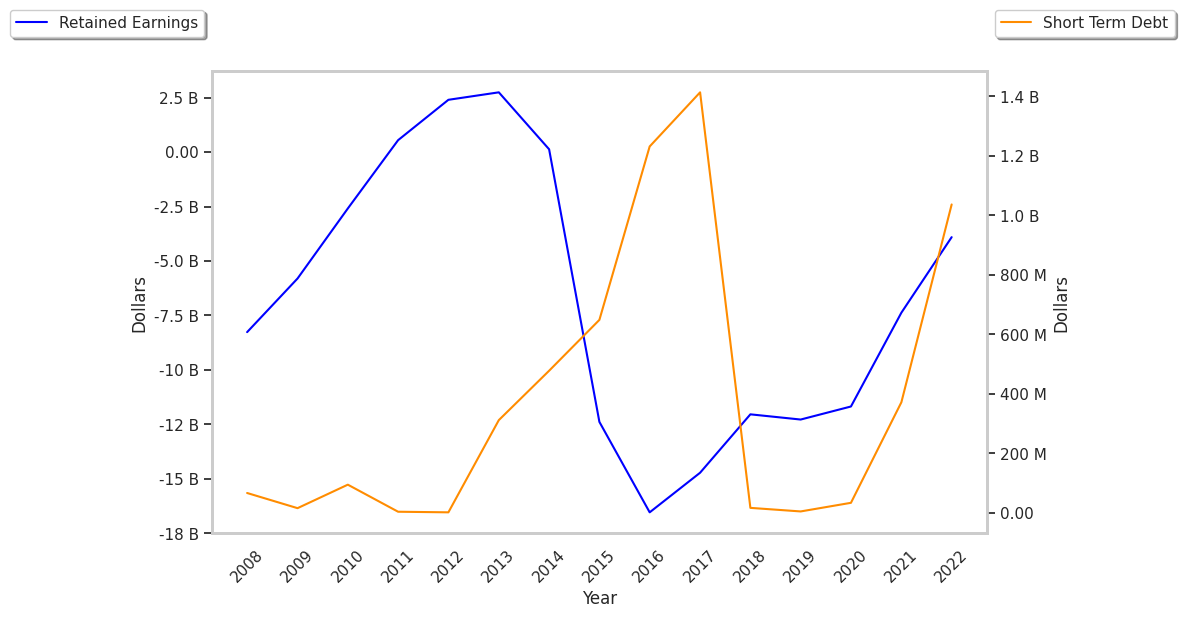

To deepen our understanding of the company's finances, we should study the effect of its depreciation and capital expenditures on the company's bottom line. We can see the effect of these additional factors in Freeport-McMoRan's free cash flow, which was $455.0 Million as of its most recent annual report. This represents the amount of money that is available for reinvesting in the business, or for paying out to investors in the form of a dividend. With its strong cash flows, FCX is in a position to do either -- which can encourage more investors to place their capital in the company. Over the last four years, the company's free cash flow has been growing at a rate of 4.7% and has on average been $1.58 Billion.

Value investors often analyze stocks through the lens of its Price to Book (P/B) Ratio (its share price divided by its book value). The book value refers to the present value of the company if the company were to sell off all of its assets and pay all of its debts today - a number whose value may differ significantly depending on the accounting method. Freeport-mcmoran's P/B ratio is 4.17 -- in other words, the market value of the company exceeds its book value by a factor of more than 4, so the company's assets may be overvalued compared to the average P/B ratio of the Basic Materials sector, which stands at 3.12 as of the second quarter of 2024.

Since it has a higher P/E ratio than its sector average, an average P/B ratio, and generally positive cash flows with a flat trend, Freeport-McMoRan is likely undervalued at today's prices. The company has poor growth indicators because of an inflated PEG ratio and decent operating margins with a positive growth rate. We hope you enjoyed this overview of FCX's fundamentals. Be sure to check the numbers for yourself, especially focusing on their trends over the last few years.