Oil & Gas Integrated company Phillips 66 is taking Wall Street by surprise today, falling to $116.74 and marking a -4.9% change compared to the S&P 500, which moved 1.0%. PSX is -17.68% below its average analyst target price of $141.81, which implies there is more upside for the stock.

As such, the average analyst rates it at buy. Over the last year, Phillips 66 has underperfomed the S&P 500 by -34.2%, moving -6.5%.

Phillips 66 operates as an energy manufacturing and logistics company in the United States, the United Kingdom, Germany, and internationally. The company is classified within the energy sector. The stock prices of energy companies are highly correlated with geopolitics: economic crisis, war, commodity prices, and politics all have an effect on the industry. For this reason, energy companies tend to have high volatility -— meaning large and frequent price swings. As global energy supplies shift towards renewables, we may see a reduced correlation between energy prices and geopolitical events.

Phillips 66's trailing 12 month P/E ratio is 14.9, based on its trailing EPS of $7.83. The company has a forward P/E ratio of 12.3 according to its forward EPS of $9.49 -- which is an estimate of what its earnings will look like in the next quarter. As of the third quarter of 2024, the average Price to Earnings (P/E) ratio for US energy companies is 13.62, and the S&P 500 has an average of 29.3. The P/E ratio consists in the stock's share price divided by its earnings per share (EPS), representing how much investors are willing to spend for each dollar of the company's earnings. Earnings are the company's revenues minus the cost of goods sold, overhead, and taxes.

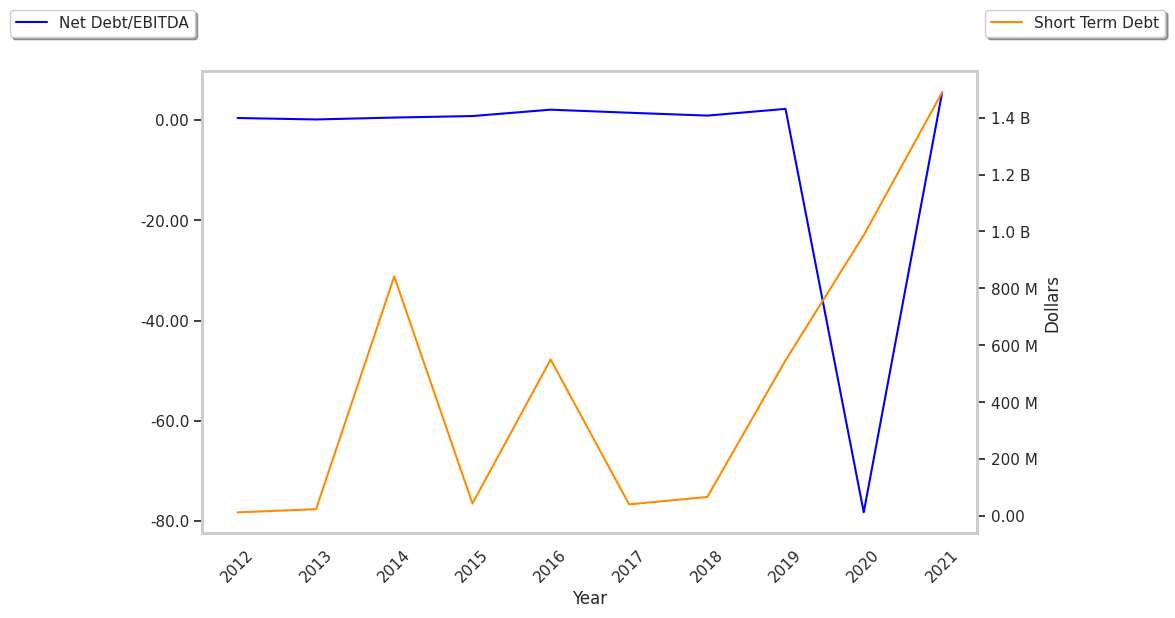

When we subtract capital expenditures from operating cash flows, we are left with the company's free cash flow, which for Phillips 66 was $4.61 Billion as of its last annual report. The balance of cash flows represents the capital that is available for re-investment in the business, or for payouts to equity investors as dividends. The company's average cash flow over the last 4 years has been $3.74 Billion and they've been growing at an average rate of -1.3%. PSX's weak free cash flow trend shows that it might not be able to sustain its dividend payments, which over the last 12 months has yielded 3.6% to investors. Cutting the dividend can compound a company's problems by causing investors to sell their shares, which further pushes down its stock price.

Another valuation metric for analyzing a stock is its Price to Book (P/B) Ratio, which consists in its share price divided by its book value per share. The book value refers to the present liquidation value of the company, as if it sold all of its assets and paid off all debts). Phillips 66's P/B ratio indicates that the market value of the company exceeds its book value by a factor of 1.68, but is still below the average P/B ratio of the Energy sector, which stood at 1.86 as of the third quarter of 2024.

Phillips 66 is likely fairly valued at today's prices because it has an average P/E ratio, an average P/B ratio, and positive cash flows with a flat trend. The stock has poor growth indicators because of its weak operating margins with a negative growth trend, and a negative PEG ratio. We hope this preliminary analysis will encourage you to do your own research into PSX's fundamental values -- especially their trends over the last few years, which provide the clearest picture of the company's valuation.